There is a reason Albert Einstein is often quoted, if somewhat questionably, as calling compound interest the eighth wonder of the world. Whether or not he said it, the math justifies the sentiment. Compound interest is the mechanism by which ordinary savers build extraordinary wealth over time. It is also the mechanism by which debt quietly grows beyond what borrowers expect. Understanding how it works on both sides of your financial life is one of the most practically valuable things you can learn about money.

Simple Interest vs Compound Interest

With simple interest, you earn returns only on your original principal. Deposit $5,000 at 5% simple interest, and you earn $250 every year, permanently, regardless of how long you leave it.

With compound interest, you earn returns on your original principal and on all the accumulated interest. In year one at 5%, your $5,000 grows to $5,250. In year two, you earn 5% on $5,250, producing $262.50. Year three, 5% on $5,512.50. The interest earns interest, and the growth accelerates over time in a way that becomes genuinely dramatic over decades.

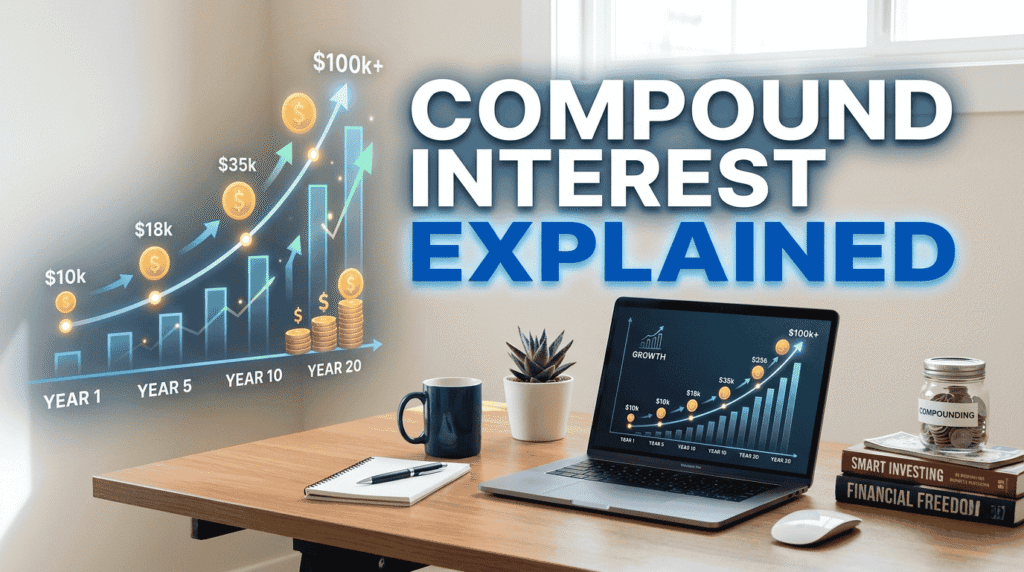

| 📊 The compounding numbers: $10,000 invested at 7% annual return, no additional contributions. Year 10 = $19,672. Year 20 = $38,697. Year 30 = $76,123. Year 40 = $149,745. The money grew $29,025 in the first 20 years and $111,048 in the second 20 years, from the same original $10,000 with no additional contributions. The acceleration is entirely the work of compounding. (Standard compound interest calculation) |

“Compound interest is the eighth wonder of the world. He who understands it, earns it. He who doesn’t, pays it.” — Attributed to Albert Einstein

Why Time Is More Powerful Than Amount

This is the insight that surprises most people when they see the actual numbers. Time is more powerful than the amount you invest or the rate of return. Starting earlier, even with smaller amounts, produces better outcomes than starting later with larger contributions.

A person who invests $5,000 per year from age 25 to 35, then stops completely, contributing $50,000 total, will typically have more at age 65 than a person who starts at 35 and invests $5,000 per year all the way to 65, contributing $150,000. Three times the money, same result or worse, because the first person had an extra decade of compounding on their initial investments.

The Rule of 72

The Rule of 72 is a simple mental shortcut for estimating how long it takes an investment to double. Divide 72 by the annual interest rate to get the approximate doubling time in years. At 6%, money doubles in roughly 12 years. At 8%, about 9 years. At 12%, about 6 years.

This simple rule makes the impact of different rates of return immediately intuitive and helps explain why small differences in investment fees matter enormously over long periods. The SEC’s free compound interest calculator lets you plug in your specific numbers to see exactly what compound growth looks like for your situation.

When Compound Interest Works Against You

Everything that makes compound interest powerful for investing makes it dangerous in debt. A credit card balance at 20% annual interest, with only minimum payments made, can take more than a decade to eliminate and cost two to three times the original balance in total interest paid. The unpaid interest is added to the principal, and that larger principal then accrues more interest. The spiral accelerates in the same way wealth does, just in the wrong direction.

This is the mathematical reason that paying off high-interest debt before investing is the right priority for most people. You cannot reliably earn 20% returns on investments. You can guarantee saving 20% by eliminating the debt charging you that rate.

For the complete debt payoff framework, our guide on how to get out of debt fast covers the sequencing and strategies in detail.

How to Maximize Compound Interest Working For You

Start as Early as Possible

Every year you wait to begin investing reduces the compounding runway available. Money invested at 25 has 40 years to compound before age 65. Money invested at 45 has 20 years. Starting imperfectly with small amounts is categorically better than waiting for the perfect amount or the perfect market moment.

Minimize Investment Fees

Investment fees directly reduce your effective rate of return, which directly reduces compounding power. A 1% annual fee sounds trivial but reduces a 40-year portfolio by approximately 25% compared to a zero-fee equivalent. This is the primary reason low-cost index funds are so consistently recommended. As NerdWallet’s expense ratio analysis explains, even small differences in fees compound into enormous differences in long-term wealth.

Reinvest All Dividends and Returns

Compounding works at maximum power when all returns are reinvested rather than withdrawn. Most investment accounts allow automatic dividend reinvestment. This single setting, often overlooked, meaningfully increases long-term returns by ensuring that every payout immediately begins compounding again.

Frequently Asked Questions

How often does compound interest compound?

It depends on the account. Most savings accounts compound daily or monthly. Investment returns compound through reinvested dividends and price appreciation over time. More frequent compounding produces slightly better results, but the difference between daily and monthly compounding on typical balances is modest.

What rate of return should I assume for calculations?

For long-term stock market investments in diversified index funds, 7% annual return after inflation is a conservative historical estimate based on S&P 500 long-term performance. For savings accounts at current rates, 4 to 5% is realistic but subject to change with economic conditions.

Why do advisors always say to start investing young?

Because of compounding. The longer the time horizon, the more periods of compounding occur, and growth in later years dwarfs earlier years. Starting at 25 versus 35 is not just ten extra years of contributions. It is ten extra years of compounding on everything invested in that window, which produces a dramatically different outcome.

Final Thoughts

Compound interest is not a complex concept, but its implications are genuinely profound. The money you put to work today is categorically more valuable than money you put to work five or ten years from now, not because of the amount, but because of the time available to compound. Understanding this changes the urgency with which you approach investing from a distant future obligation to the most time-sensitive financial decision in front of you right now.

For the investment vehicles that put compound interest to work most effectively, our guide on what are index funds and should you invest in them covers the most widely recommended approach for individual investors.